When you utilize a system that works you should continue to use it. That is a pretty straightforward statement. My personal returns have been less than optimal in the last month, but it’s not the fault of T-Theory itself. When using a system that is entirely invested in an asset during a T, the individual’s level of acceptance of risk is extremely important, and mine has been extremely low. We may be near the end of “Outcome Failures”, but being conservative certainly aided in strategy this year.

Since my October 1 post, I was looking for a bottom around middle October. We achieved that.

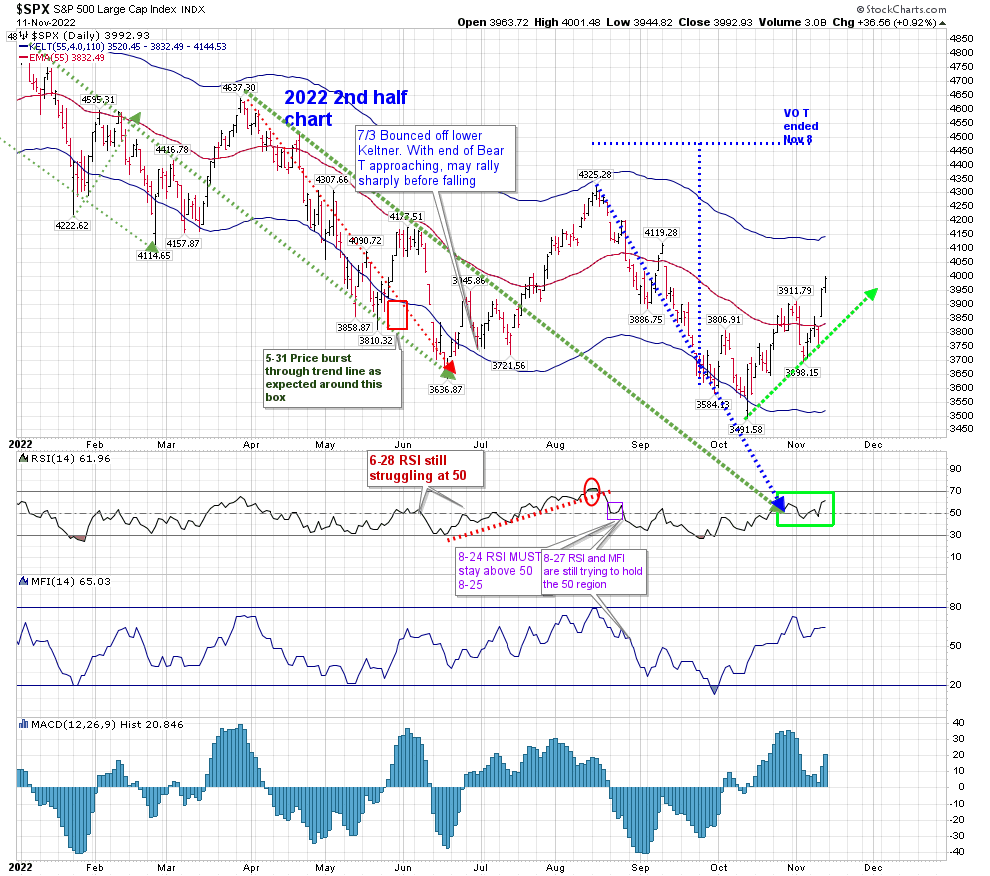

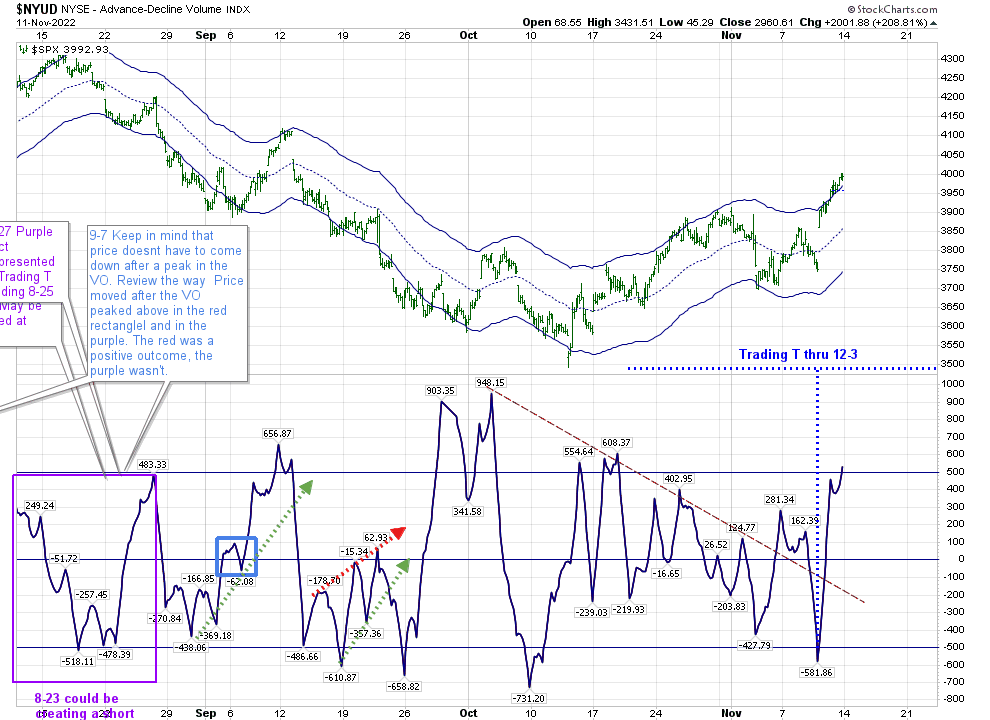

By the middle of October we went above the zero line, and stayed there, even with all the 150-200 point moves both up and down that have occurred almost every week for the last 3 weeks. The end of the November 8 T gave us a peak at 3860, before losing over 100 points to 3744. But a surprising thing happened. RSI has not gotten much below 50 since early this month, following through on last week’s post.

That very sharp drop on November 9 didn’t create a negative outcome. The VO didn’t cross below the zero line when we hit 3744—it reversed.

This creates the possibility for an extended period of strength in the market. The possibility is that we have a T that lasts through January 22. I am not marking that on the official T Chart at this time. It is created by beginning the left side of the T on May 27, with a center point of September 23, and a concluding date in January.

The two Bear T’s that occurred during this T (shown on the marked T-Theory Chart) lead me to reject it at the moment.

But that doesn’t mean we aren’t in a Positive environment. We have a Trading T that extends through December 3, as noted on the hourly Chart:

Support for this T is 3857. We are above the upper Keltner of 3970, and that is acting as our first level of support at this time. RSI should manage to stay above 50 as additional support. A failure of 50 to hold on the hourly rate would create caution.

Back in May, I posted regarding the concept of Snowflakes–market moves being unique, but perhaps with ‘cousins’. Most people look at the 1929-32 market as being one 89% move down. Carl Swenlin pointed out in an article there were really 6 bear and five bull markets inside that drop, if you take a move of 20% as representative of those nomenclatures.

The article can be found here:

https://stockcharts.com/articles/decisionpoint/2022/05/those-who-do-not-learn-from-hi-954.html

Are we in one of those Bull moves within a larger Bear? While the question has to be asked, I can only give you my personal point of view–we can have Positive Outcomes within a longer term Bearish scenario. Right now, we’re in that Positive Period whether it’s long term or short term. I’ve been wary of this market since January, and that served me well, as I hope it’s done for you.

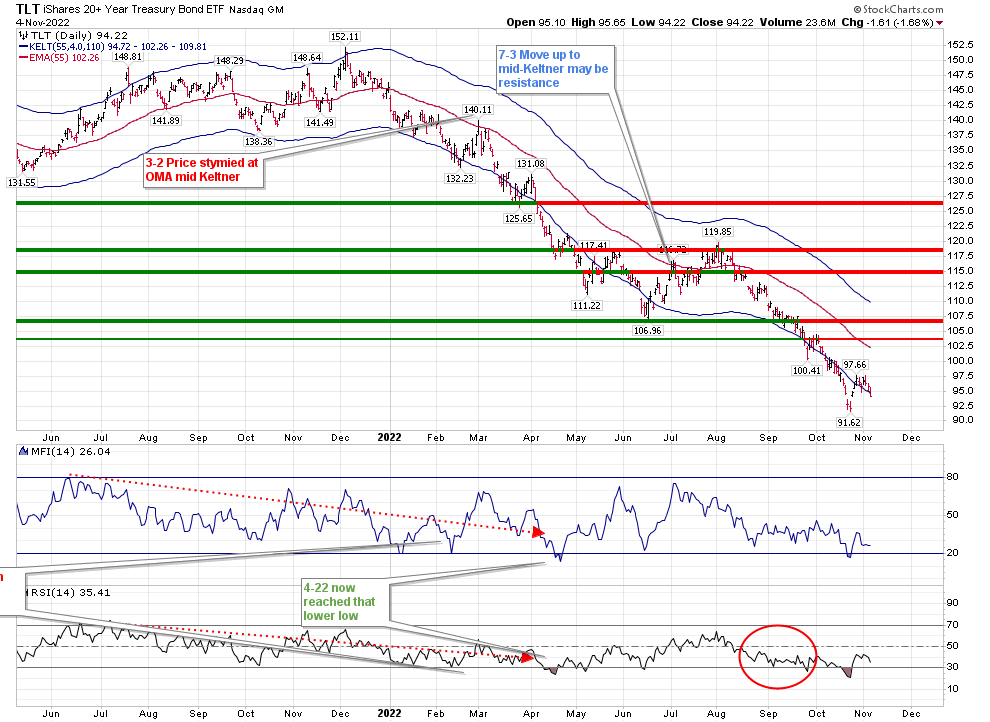

I am ‘trading’ this T using VCIT, a corporate bond ETF as my surrogate for equities. It was common practice (until yields went to ridiculous lows) to be in either corporate or treasury funds rather than equities for the duration of a T. Terry Laundry called this the “Best Bond” strategy. Now that rates have increased substantially, I am utilizing that strategy for this particular T. The T on this can be found in the “Existing T” portion of the site menu.

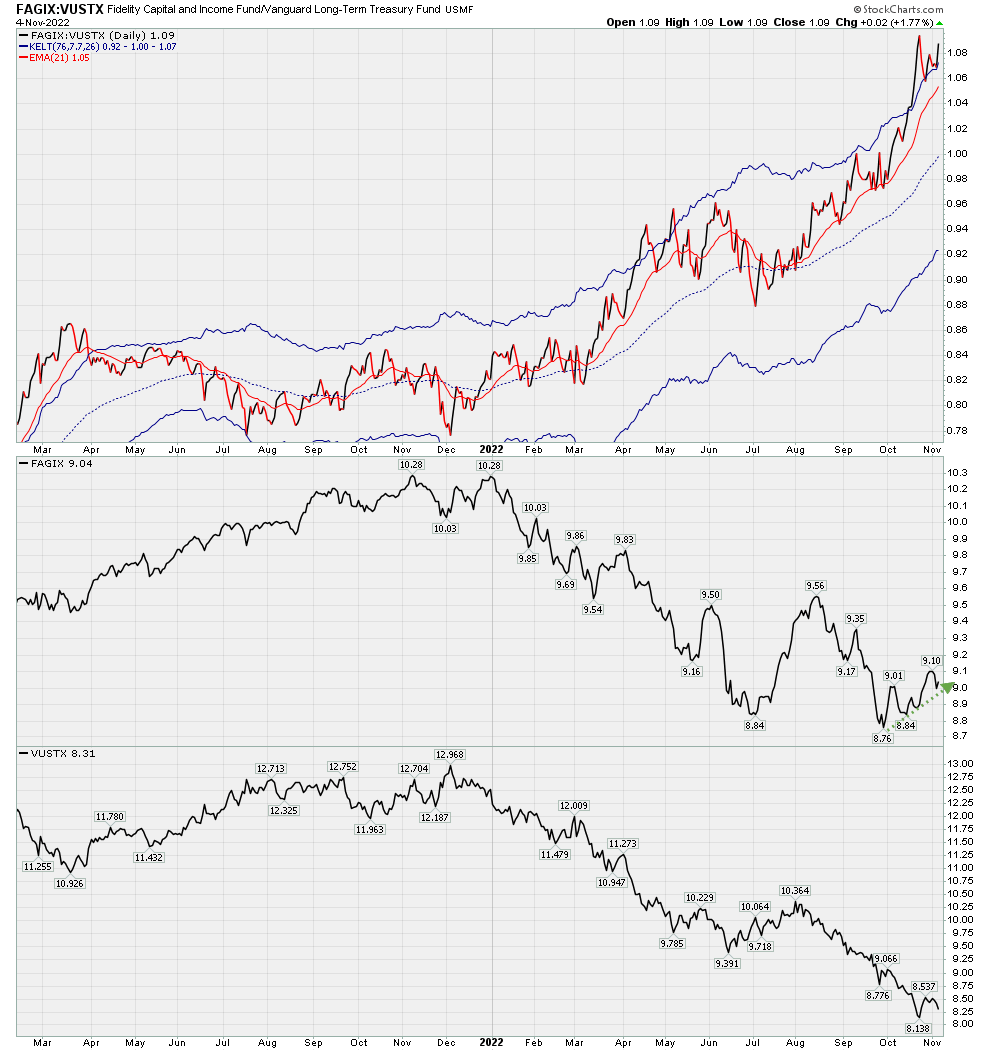

The fact that I am invested in Corporate bonds may appear to be in conflict with my comments regarding the Confidence Index being overbought. But the chart of many of the Investment Grade Corporate bonds look so much better than those of similar Treasury Bond ETFs.

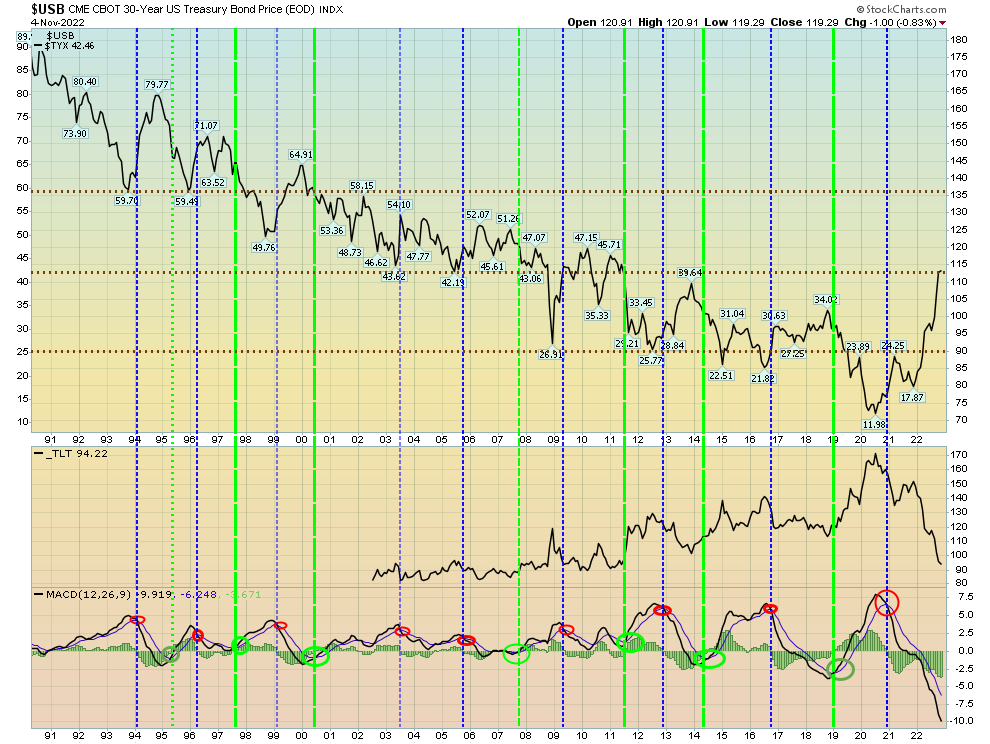

The 10 Year is back where it was a month ago. In my October 23 report I outlined the peak in rates also created peaks in RSI and MACD. They have since been followed by lower peaks, as noted on the chart. I expect one more swing higher in rates as we come to the culmination of this T in 2 weeks.

Rates are normally very slow to move, and slower to turn directions. This recent period of bond volatility should stabilize soon.