The XOM T should have completed a period of strength yesterday. Instead, it brought the potential for a strong move lower next week.

This T had a center point of July 20. It was a strong area of support based on price, RSI, and MFI lows against their respective bands.

It was evident that XOM could not crack through its middle Keltner, nor 50 on the two technical indicators. When price dropped below 53, this structure became a Bear T. A Bear T has a lower low than the center point of the T. Near the end of the T, there is usually a rally from Hell, which is followed by a price collapse. That is the expected outcome at this point. I think XOM has shown all the ingredients of this potential.

Unfortunately we have the potential of a hurricane passing through the Gulf, which is both alarming on a humanitarian level, and may have an impact on the future of the chart. I can only account for what the chart tells me.

With the “Weak T” on the McOsi ending September 3, the outlook for equities is in jeopardy. (Please ignore the last VO reading as StockCharts hasn’t updated it yet.) The McOsi has peaked at the same level as the last descending high trend line, unless Monday’s action moves it higher.

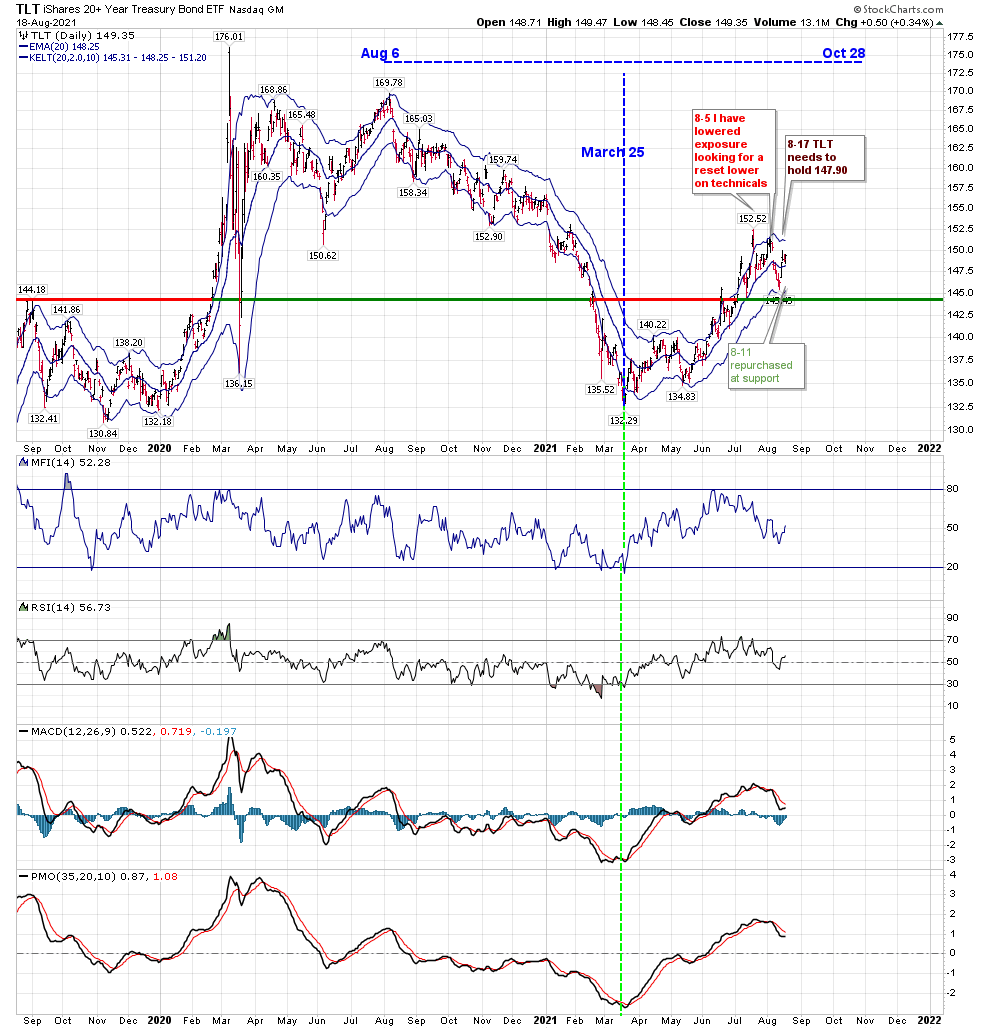

As for the T in TLT, we have stayed within the 144-151 range I have suggested. For those who follow me through Avi Gilburt’s site, you know that I sold calls around this week’s high, and repurchased them around 148, the day before Jackson Hole. While this enabled me to regain some of the reduction in price, it didn’t cover it fully. These were ITM options, which moved to OTM, leaving time premium.

It’s become clearer to me as to how the T in the Ten Year Bond can exist as well as the T in TLT. This T can continue to result in higher rates, which longer term bond holders may accept as helping to keep long term rates lower for longer. I will shortly be taking a converse position on IEF or use some other vehicle. I don’t intend to post on that position.

Below is a chart showing the asset class performance since the T in TLT was discovered. Returns were increased by successfully trading my TLT position.

IWM has shown a surprising amount of strength recently. Its value has returned to 50.03% of SPY.

It is still below the resistance level on this chart. Watch for a breakthrough.

Have a safe and enjoyable Labor Day. I don’t expect to post before then. This is a copy of the present chart before I remove some old comments and lines: